MARCH 30, 2023

Mortgage Rates Hit Lowest Level in 6 Weeks

By Matt Ott

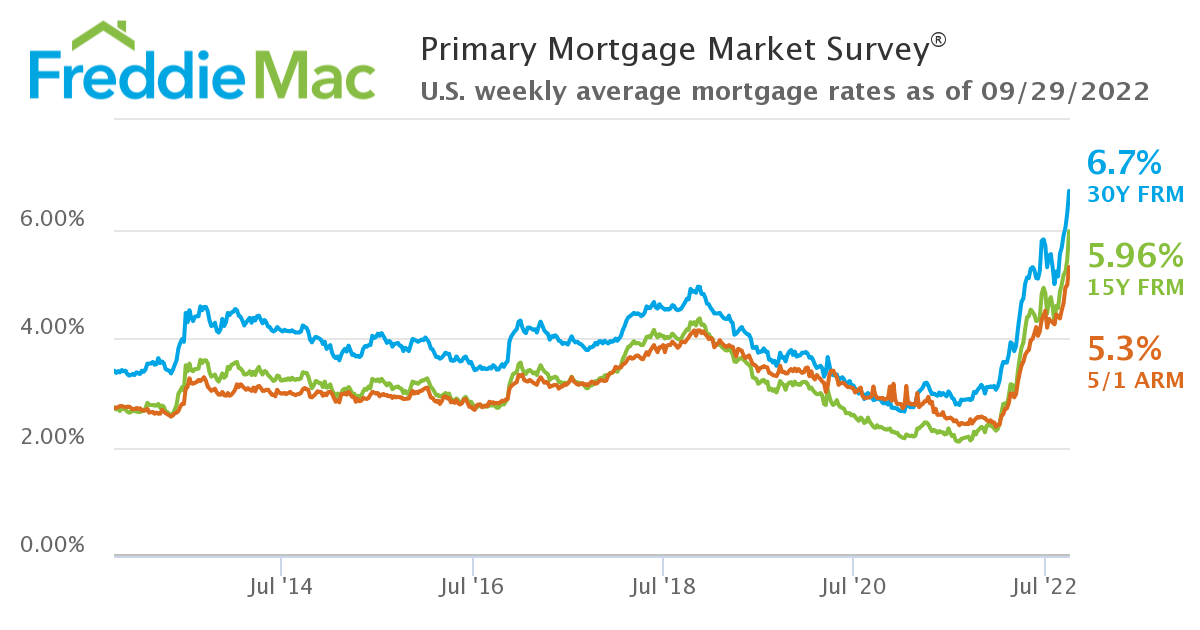

At 6.32%, the average 30-year, fixed-rate mortgage declined from last week’s average 6.42% – a ray of hope for buyers seeking to secure a home this spring.

WASHINGTON – The average long-term U.S. mortgage rate inched down this week to its lowest level in six weeks, just as the spring buying season gets underway.

Mortgage buyer Freddie Mac reported Thursday that the average on the benchmark 30-year rate fell for the third straight week to 6.32%, from 6.42% last week. The average rate a year ago was 4.67%.

The recent decline in mortgage rates is good news for prospective homebuyers, as many were pushed to the sidelines during the past year as the Federal Reserve cranked up its main borrowing rate nine straight times in a bid to bring down stubborn, four-decade high inflation.

Also helping buyers, home prices appear to be leveling off. The national median home price slipped 0.2% from February last year to $363,000, marking the first annual decline in 13 years, according to the National Association of Realtors.

One thing that hasn’t gotten much better is the supply of homes.

“Over the last several weeks, declining rates have brought borrowers back to the market, but as the spring home buying season gets underway, low inventory remains a key challenge for prospective buyers,” said Sam Khater, Freddie Mac’s chief economist.

Rising borrowing costs can add hundreds of dollars a month in costs for homebuyers and put the brakes on the housing market. Before surging 14.5% in February, sales of existing homes had fallen for 12 straight months to the slowest pace in more than a dozen years.

In 2022, existing U.S. home sales fell 17.8% from 2021, the weakest year for home sales since 2014 and the biggest annual decline since the housing crisis began in 2008, the National Association of Realtors reported earlier this year.

The average long-term rate hit 7.08% in the fall – a two-decade high – as the Federal Reserve quickly cranked up its key lending rate with multiple jumbo hikes in a bid to cool the economy and stymie persistent, four-decade high inflation.

In their latest quarterly economic projections, the policymakers forecast that they expect to raise that key rate just once more – from its new level of about 4.9% to 5.1%, the same peak they had projected in December.

While the Fed’s rate hikes do impact borrowing rates across the board for businesses and families, rates on 30-year mortgages usually track the moves in the 10-year Treasury yield, which lenders use as a guide to pricing loans. Investor expectations for future inflation, global demand for U.S. Treasurys and what the Federal Reserve does with interest rates can also influence the cost of borrowing for a home.

Treasury yields have fluctuated wildly since the collapse of two mid-size U.S. banks two weeks ago. The yield on the 10-year Treasury, which helps set rates for mortgages and other important loans, was 3.57% Thursday, but had been above 4% early in March.

The rate for a 15-year mortgage, popular with those refinancing their homes, fell this week to 5.56% from 5.68% last week. It was 3.83% one year ago.

Copyright 2023 The Associated Press. All rights reserved. This material may not be published, broadcast, rewritten or redistributed without permission.

![Experts Agree: Options Are Improving for Buyers [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2021/07/15150442/20210716-MEM-1046x1908.png)