This week, Chief Economist Danielle Hale discusses what small business optimism, consumer and producer inflation data, and retail sales data signal about the U.S. economy. She also highlights what these data imply for the Fed’s likely path forward.

0:10 – Business optimism trends

0:25 – Inflation trends

1:24 – Mortgage rates

1:40 – Construction trends

2:11 – Real estate listings trends

At 6.14%, Weekly Mortgage Rates Hit Sept. Lows

JANUARY 19, 2023

It’s down from last week’s 6.33%. Freddie Mac’s chief economist says it provides a “much-needed boost” for the housing market, but inventory is a concern.

Copyright 2023 The Associated Press. All rights reserved.

WASHINGTON (AP) – The average long-term U.S. mortgage rate fell this week to its lowest level since September, a potential boost to the housing market which has been in decline for nearly a year.

Mortgage buyer Freddie Mac reported Thursday that the average on the benchmark 30-year rate fell to 6.15% from 6.33% last week. A year ago the average rate was 3.56%.

The average long-term rate reached a two-decade high of 7.08% in the fall as the Federal Reserve continued to boost its key lending rate in its quest to cool the economy and tame inflation.

The big rise in mortgage rates during the past year has throttled the housing market, with sales of existing homes falling for 10 straight months to the lowest level in more than a decade.

Though home prices have retreated as demand has declined, they are still nearly 11% higher than a year ago. Higher prices and a doubling of mortgage rates have made homebuying much less affordable for many people, but recent rate declines could give some homebuyers new hope.

“Rates are at their lowest level since September of last year, boosting both homebuyer demand and homebuilder sentiment,” said Sam Khater, Freddie Mac’s chief economist. “Declining rates are providing a much-needed boost to the housing market, but the supply of homes remains a persistent concern.”

At its final meeting of 2022, the Federal Reserve raised its rate 0.50 percentage points, its seventh increase last year. That pushed the central bank’s key rate to a range of 4.25% to 4.5%, its highest level in 15 years.

Though inflation at the consumer level has declined for six straight months, Fed officials have signaled that they may raise the central bank’s main borrowing rate another three-quarters of a point in 2023, which would be in a range of 5% to 5.25%.

Rates for 30-year mortgages usually track the moves in the 10-year Treasury yield, which lenders use as a guide to pricing loans. Investors’ expectations for future inflation, global demand for U.S. Treasurys and what the Federal Reserve does with interest rates can also influence the cost of borrowing for a home.

The rate for a 15-year mortgage, popular with those refinancing their homes, also declined this week, to 5.28% from 5.52% last week. It was 2.79% one year ago.

Real Estates Current Market Silver Lining

For those looking for the good news about today’s real estate market. A bit of a deep dive, about 60 minutes worth but excellently delivered. Three main facts tell us it’s not all doom and gloom. Combine them with the time of year and the general fear that has most buyers/sellers on the sidelines, spells opportunity. (40:00). We can help should you decide to take advantage of today’s market.

- Historical trends, what happens after quantitative tightening (12:00)

- Demographics, there’s a lot of millennials (24:50)

- Inventory levels, yes they are still historically low (22:00)

First-time Buyers Back Despite Challenges

They now make up 45% of all homebuyers, up from 37% last year, even as affordability issues persist. Repeat buyers may have pulled back due to rising interest rates.

CHARLOTTE, N.C. – First-time home buyers have returned to the housing market, and those who can afford a home are finding success after years of setbacks. The share of buyers purchasing a home for the first time has rebounded to pre-pandemic levels.

First-time buyers now represent 45% of all buyers, up from 37% of buyers surveyed last year, according to Zillow’s 2022 Consumer Housing Trends Report. If they can overcome affordability challenges, first-time buyers could be well positioned to continue increasing their share in today’s shifting market, with more options and time to decide on the right home.

The share of first-time buyers plummeted during the pandemic amid rapidly rising home values and tough competition, even with high demand coming from the large millennial generation. Zillow research found younger, likely first-time shoppers were losing out to older, repeat buyers who were able to tap the equity in their existing homes and use cash to make a stronger offer. A Zillow survey found younger buyers were more likely to report losing to an all-cash buyer at least once, as was the case for 45% of Gen Z and 38% of millennial buyers, compared to 30% of all buyers.

“First-time buyers now appear to be making relative gains as high mortgage interest rates disproportionately encourage current homeowners to stay put,” said Zillow population scientist Manny Garcia. “The flow of homes into the market is slowing, suggesting homeowners are likely comparing their current low mortgage rate to today’s rates and deciding not to move. While rising mortgage rates are hurting affordability for all buyers, first-time buyers may be less deterred by higher rates because they’re comparing a monthly mortgage payment to what they’re paying in rent.”

First-time buyers are making up a larger share of a smaller pie. Newly pending home sales were down 29% in August, compared to a year prior, as buyers struggle to keep up with higher home prices and interest rates. Home values remain 14.1% higher than last year, even after two consecutive month-over-month declines. When combined with rising mortgage interest rates, the typical monthly payment on a home is nearly 60% higher today than it was a year ago.

Recent Zillow research finds those affordability challenges have driven up demand for the lowest-priced homes in each market. While there are fewer buyers overall, first-time buyers may find more competition for starter homes.

The silver lining is that today’s much-needed market rebalancing has the potential to especially benefit first-time buyers, who have the flexibility to shop without trying to time the purchase of their new home with the sale of an existing home. Listings typically lingered 16 days on the market in August before going under contract, compared to eight days in June, meaning buyers have twice as much time to decide on a home compared to this time last year.

First-time buyers may also have more bargaining power as a growing number of sellers drop their prices. The share of listings with a price cut grew to roughly 28% in August, according to Zillow’s latest monthly market report.

As the market changes, aspiring first-time buyers may need to change their approach. These five tips are a good starting point:

- Understand what’s affordable. As mortgage interest rates fluctuate, aspiring buyers can start with a mortgage calculator to understand what they can realistically afford on a monthly basis. Take into account some of the hidden costs of homeownership, such as property tax, insurance and HOA dues, which can add up to more than $750 per month. But it’s always best to leave some wiggle room in the budget for unexpected maintenance projects and emergency repairs. First-time shoppers should also explore down payment assistance programs they may qualify for.

- Finance first. First-time buyers can gain a competitive edge by getting pre-approved for a mortgage. A Zillow survey finds 86% of sellers prefer a buyer who has been pre-approved, as opposed to pre-qualified, for a mortgage. This financial check gives sellers more certainty that a buyer will close on time, and it allows buyers to make a stronger, faster offer the minute the right home hits the market. Buyers can start the pre-approval process online. Don’t hesitate to try, try, try again. Nearly half of all first-time buyers (47%) are denied a mortgage at least once before ultimately getting approved.

- Hire the right agent. An experienced agent will have a finger on the pulse of their local market and know all the changes happening in it, and they can help buyers make strategic decisions to win. They’ll know when to come in with an offer under list price or when to expect a bidding war. Buyers should plan on interviewing their top candidates and asking the right questions.

- Shop smarter with tech. New real estate technology can help first-time buyers make faster, smarter decisions. Virtual 3D Home tours and interactive floor plans give shoppers a more authentic experience of a home, allowing them to quickly narrow down their options and tour fewer homes in person.

- Keep the contingencies. With less competition, first-time buyers should have the leverage to include important contingencies in their offers that could potentially save them a lot of money in the long run. An inspection contingency can identify major structural, mechanical or safety issues that could be extremely costly to repair and cause buyer’s remorse. A financing or appraisal contingency will ensure a buyer can walk away with their earnest money if a home fails to be appraised for the offer price or if their financing falls through.

Copyright © 2022 BridgeTower Media and © 2022, The Mecklenburg Times (Charlotte, NC). All rights reserved.

Weekly Market Report: Week Ending Oct. 16

Access this weekly report for real-time data on residential market activity across the Bright MLS footprint.

October 17, 2022 Lisa Sturtevant, PhD

Here are the highlights for the week ending October 16, 2022:

- Inventory continues to increase throughout the Bright footprint. The average number of active listings during the week ending October 16 was up 17.5% compared to the same week a year ago. Active listings edged up 0.9% compared to last week, which is the second weekly increase in a row. Despite these increases, overall supply across the region remains very low.

- Market activity is still below 2019 levels as buyers and sellers continue to remain on the sidelines. On the buyer side, both closed sales and new purchase contracts were down significantly compared to last year at this time and were even lower than before the pandemic. Closed sales this week were about 14% lower than the same week during 2019, while the number of new purchase contracts tracked 22% lower than during the same week in 2019.

- There was a slight uptick in both new purchase activity and new listings compared to a week ago. Typically, both the number of new purchase contracts and new listings decline during the second week of October. This year, however, there were slight increases, with new purchase contracts 2.1% higher than a week ago and new listings up 3.0% week-to-week. These weekly increases could indicate some buyers and sellers are starting to act in anticipation of higher mortgage rates later this fall.

- Homes are still selling relatively quickly. The median days on market was 15 during the week ending October 16, which is up four days compared to last year and is one day longer than a week ago. The median days on market is still much lower than 2019, when homes typically took 25 days to sell.

Scott Bradley Brixen – ListReports Blog

Real Estate News

Interest rates for the average 30-yr, fixed-rate mortgage according to Freddie Mac’s PMMS hit:

4% in March 😟

5% in April 😰

6% in early-September 😨

7% (well, almost) in late-September 😱

The slowdown continues, but we have yet to see the impact of the most recent (massive) jump in mortgage rates on homebuyer demand.

August existing home sales dropped for the 7th straight month. Price growth decelerated further to “just” 8% YoY. [Source: Realtor.com]

Meanwhile, pending sales for August dropped 2% MoM and 24% YoY. The NAR now forecasts existing home sales to fall 15% YoY in 2022, with new home sales down 21% YoY. [Source: NAR]

Case-Shiller Index

Home price growth slowed to 15.8% YoY in July, from 18.1% YoY in June. That may not seem like much, but it’s the biggest 1-month drop in the index’s history.

Case-Shiller is the gold standard for home price appreciation because it tracks the sales prices of very similar homes across 20 big cities. It’s an ‘apples to apples’ comparison. But that accuracy comes at a cost…the data is 2 months old by the time we get it.

Mortgage Market

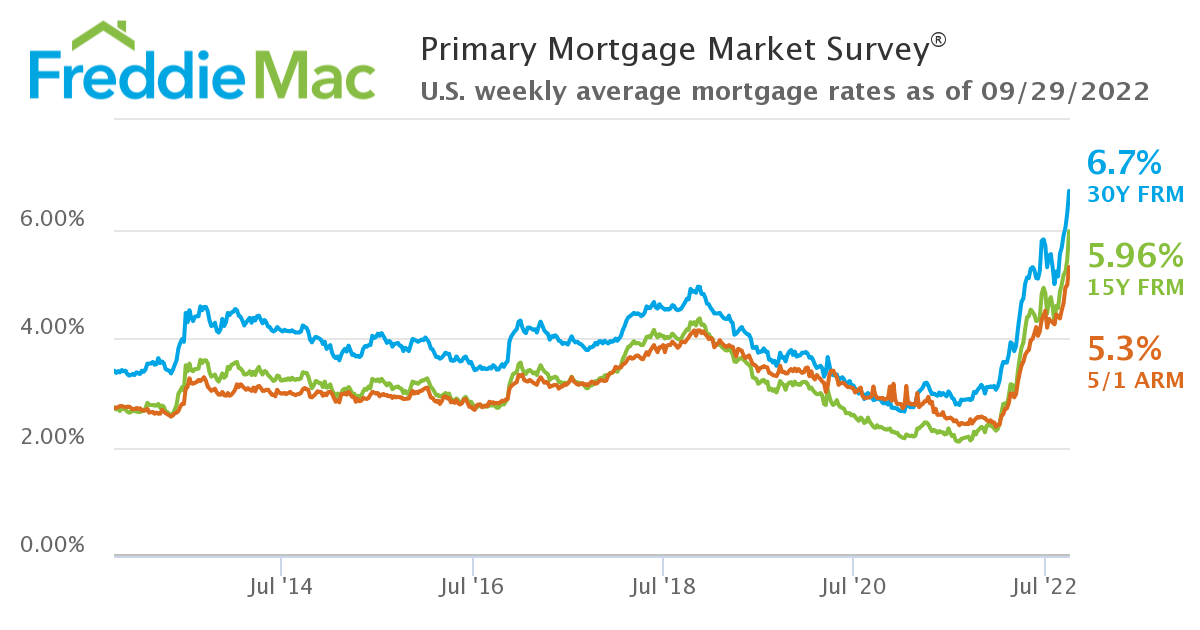

An extremely volatile week for the bond market (after the Fed raised rates 75bps) saw 30-year, fixed-rate mortgages briefly exceed 7% [with no points], before dropping back to around 6.75%. [Source: Mortgage News Daily]

Freddie Mac’s closely watched PMMS survey saw the interest rate on the average 30-year, fixed-rate mortgage climb to 6.7%. Keep in mind that this figure includes an average 0.9 points purchased. Without those points, the rate would have been at/ahead of 7%.

Still a Seller’s Market

Demand is falling and inventory has risen, but in most markets, well-priced homes are still selling very, very quickly.

In fact, the average Days on Market for sold properties has only edged up from 14 (in June & July) to 16 in August. In 2011 that figure was 96! Looked at another way, 81% of homes sold in August had been on the market less than a month.

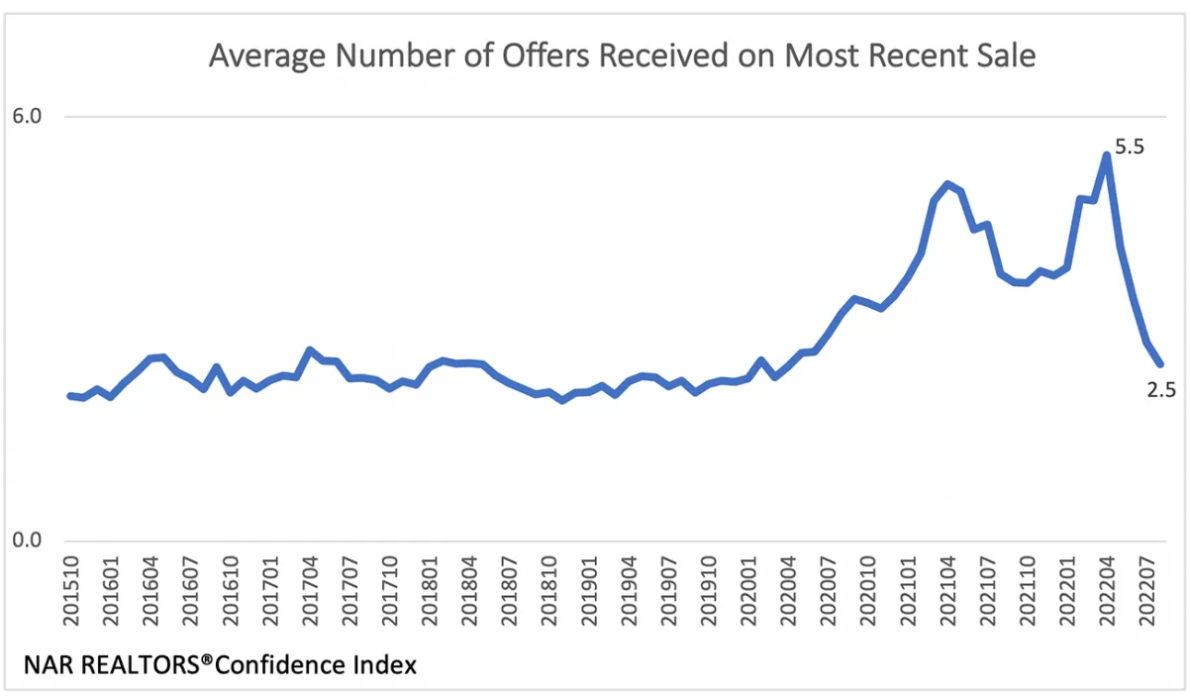

That said, the average number of offers received for each property sold has plunged from a frenzied 5.5 in April 2022 to 2.5 in August. That’s actually getting pretty close to “normal” pre-pandemic levels of competition.

National Housing Stats

They Said It

“Success demands singleness of purpose. You need to be doing fewer things for more effect instead of doing more things with side effects. It is those who concentrate on one thing at a time who advance in this world.” — Gary Keller, The One Thing

“Our house is clean enough to be healthy and dirty enough to be happy” — Robyn Griggs Lawrence

Inspiration

The average duration of homeownership in the US is around 12 years. So if someone in your sphere of influence (SOI) bought a home in the last few years, there’s no reason to actively stay in touch with them, right? Wrong. Take the inverse of 12 (that’s 1/12) and you get 8.3%.

This means that, mathematically, 8% of your SOI is going to move in the next year…for reasons that you (and often they) couldn’t have predicted. Hockey legend Wayne Gretzky said “you miss 100% of the shots you don’t take.” In real estate, you probably lose 80–90% of the past clients that you don’t stay in contact with.

As the Federal Reserve raised its key interest rate Wednesday, what does it mean for home sellers and buyers?

Weekly Housing Market Update – 9/16/22 – Chief NAR Economists, Danielle Hale, not only forecasted the rate hike she also highlights her thoughts around 2:35 of the video regarding home sellers and home buyer.

August 2022 Monthly Housing Market Trends Report

Sabrina Speianu, Economic Data Manager, realtor.com®

- The national inventory of active listings increased by 26.6% over last year.

- The total inventory of unsold homes, including pending listings, increased by just 1.3% year-over-year due to a decline in pending inventory (-21.9%).

- Selling sentiment declined and listing activity followed, with newly listed homes declining by 13.4% on a year-over-year basis.

- The median list price grew by 14.3% in August, a deceleration from recent highs.

- Time on market was 42 days, 5 days more than last year but 22 days less than typical pre-pandemic levels.

- Regionally, large Western markets which saw some of the most growth last year and earlier this year are now showing the greatest signs of deceleration, with larger inventory increases, more price reductions, and more quickly decelerating price growth than other regions.

NAR Chief Economist Addresses Senate Committee

JULY 22, 2022

By Kerry Smith

Sales will weaken and for-sale inventory will grow, but it won’t do much to help affordability, Chief Economist Lawrence Yun said.

WASHINGTON – National Association of Realtors® (NAR) Chief Economist Lawrence Yun spoke before the U.S. Senate Committee on Banking, Housing and Urban Affairs as they dig deeper in an attempt to understand what’s happening in the U.S. housing market.

Yun told the committee that he doesn’t foresee a nationwide decline in home prices despite indications that price growth is set to slow. He testified that the potential for weaker sales should increase available for-sale inventory in some markets, but not enough to diminish persistent affordability constraints that, for many Americans, have kept homeownership out of reach for years.

“In the near term, I do not expect the situation to change appreciably,” Yun said Thursday. “Historic undersupply in the market, combined with continued demand, will likely drive ongoing issues with affordability for many Americans.

“Any short-term price adjustments, if they occur, will be less consequential compared to the immense longer-term housing affordability challenges we face as a country.”

Thursday’s hearing, Priced Out: The State of Housing in America, was recorded and can be viewed online.

The committee hearings come as the nation confronts a 6-million-unit housing shortage. The decades-in-the-making phenomenon has helped sustain year-over-year price growth for a record 124 consecutive months. A study of other circumstances influencing the market is also particularly compelling given COVID’s impact on U.S. housing and the more recent fluctuations in mortgage interest rates.

“When the Federal Reserve essentially went all-in in the early months of the pandemic … the decline in mortgage rates and the cautious reopening of the economy boosted housing demand,” said Yun. “The housing market always responds to changes in mortgage rates.”

Interest rates, which had been consistently in the 4-to-5% range in the decade preceding COVID-19, hovered near record lows of around 3% throughout much of 2020 and 2021. NAR’s most recent existing home sales report found that the average commitment rate for a 30-year, conventional, fixed-rate mortgage in June was up to 5.52%.

“Any increases in available inventory observed over the first half of this year have been offset by the corresponding increases in consumer costs,” Yun said on Capitol Hill, explaining that rate increases of roughly 2.5 percentage points have added about $800 per month to a median-priced house payment.

“This affordability crunch is felt most acutely as we move down the income scale and by minority households, given the current income distribution in America,” he continued. “That is why housing supply must be addressed to moderate home price and rent gains.”

© 2022 Florida Realtors®

Existing-Home Sales Retract 2.4% in April

May 19, 2022

Media Contact: Quintin Simmons 202-383-1178

Key Highlights

- Existing-home sales fell for the third straight month to a seasonally adjusted annual rate of 5.61 million. Sales were down 2.4% from the prior month and 5.9% from one year ago.

- With slower demand, the inventory of unsold existing homes climbed to 1.03 million by the end of April, or the equivalent of 2.2 months of the monthly sales pace.

- The median existing-home sales price increased at a slower year-over-year pace of 14.8% to $391,200.

“Higher home prices and sharply higher mortgage rates have reduced buyer activity,” said Lawrence Yun, NAR’s chief economist. “It looks like more declines are imminent in the upcoming months, and we’ll likely return to the pre-pandemic home sales activity after the remarkable surge over the past two years.”

Read full NAR article