It’s down from last week’s 6.33%. Freddie Mac’s chief economist says it provides a “much-needed boost” for the housing market, but inventory is a concern.

Copyright 2023 The Associated Press. All rights reserved.

WASHINGTON (AP) – The average long-term U.S. mortgage rate fell this week to its lowest level since September, a potential boost to the housing market which has been in decline for nearly a year.

Mortgage buyer Freddie Mac reported Thursday that the average on the benchmark 30-year rate fell to 6.15% from 6.33% last week. A year ago the average rate was 3.56%.

The average long-term rate reached a two-decade high of 7.08% in the fall as the Federal Reserve continued to boost its key lending rate in its quest to cool the economy and tame inflation.

The big rise in mortgage rates during the past year has throttled the housing market, with sales of existing homes falling for 10 straight months to the lowest level in more than a decade.

Though home prices have retreated as demand has declined, they are still nearly 11% higher than a year ago. Higher prices and a doubling of mortgage rates have made homebuying much less affordable for many people, but recent rate declines could give some homebuyers new hope.

“Rates are at their lowest level since September of last year, boosting both homebuyer demand and homebuilder sentiment,” said Sam Khater, Freddie Mac’s chief economist. “Declining rates are providing a much-needed boost to the housing market, but the supply of homes remains a persistent concern.”

At its final meeting of 2022, the Federal Reserve raised its rate 0.50 percentage points, its seventh increase last year. That pushed the central bank’s key rate to a range of 4.25% to 4.5%, its highest level in 15 years.

Though inflation at the consumer level has declined for six straight months, Fed officials have signaled that they may raise the central bank’s main borrowing rate another three-quarters of a point in 2023, which would be in a range of 5% to 5.25%.

Rates for 30-year mortgages usually track the moves in the 10-year Treasury yield, which lenders use as a guide to pricing loans. Investors’ expectations for future inflation, global demand for U.S. Treasurys and what the Federal Reserve does with interest rates can also influence the cost of borrowing for a home.

The rate for a 15-year mortgage, popular with those refinancing their homes, also declined this week, to 5.28% from 5.52% last week. It was 2.79% one year ago.

Home prices rose 8.6% in 3Q, with 46% of metros seeing double-digit price growth – a drop from 80% in 2Q. Of the top 10 high-price-increase metros, 7 are in Fla.

WASHINGTON – An overwhelming majority of metro markets saw home price gains in the third quarter of 2022, according to the National Association of Realtors® (NAR). That increase was in spite of rising mortgage rates that approached 7% and declining sales.

Of the 185 metros NAR tracks, 46% had double-digit price increases, though that’s down from 80% in the second quarter.

The national median single-family existing-home price climbed 8.6% year-to-year to $398,500. While still a notable price increase, it’s down from the 14.2% recorded in the previous quarter.

“Much lower buying capacity has slowed home price growth and the trend will continue until mortgage rates stop rising,” says NAR Chief Economist Lawrence Yun. “The median income needed to buy a typical home has risen to $88,300 – that’s almost $40,000 more than it was prior to the start of the pandemic back in 2019.”

Among the major U.S. regions, the South registered the largest share of single-family existing-home sales (44%) and the greatest year-over-year price appreciation (11.9%) in the third quarter. Prices were up 8.2% in the Northeast, 7.4% in the West, and 6.6% in the Midwest.

Fla. has 7 of top 10 metros for price growth

North Port-Sarasota-Bradenton – 23.8%

Lakeland-Winter Haven – 21.2%

Myrtle Beach-Conway-North Myrtle Beach, S.C.-N.C. – 21.1%

Panama City – 20.5%

Deltona-Daytona Beach-Ormond Beach – 19.6%

Port St. Lucie – 19.4%

Greenville-Anderson-Mauldin, S.C. – 18.9%

Kingsport-Bristol-Bristol, Tenn.-Va. – 18.8%

Tampa-St. Petersburg-Clearwater – 18.8%

Ocala (18.8%

10 most expensive markets in the U.S.

San Jose-Sunnyvale-Santa Clara, Calif. – $1,688,000; 2.3%

San Francisco-Oakland-Hayward, Calif. – $1,300,000; -3.7%

“The more expensive markets on the West Coast will likely experience some price declines following this rapid price appreciation, which is the result of many years of limited home building,” Yun says. “The Midwest, with relatively affordable home prices, will likely continue to see price gains as incomes and rents both rise.”

Higher cost for monthly payments

In the third quarter of 2022, stubbornly high home prices and increasing mortgage rates reduced housing affordability. The monthly mortgage payment on a typical existing single-family home with a 20% down payment was $1,840. That’s a marginal increase from the second quarter ($1,837) but a significant year-to-year jump of $614 – or 50%.

Families typically spent 25% of their income on mortgage payments, down from 25.3% in the prior quarter, but up from 17.2% one year ago.

“A return to a normal spread between the government borrowing rate and the home purchase borrowing rate will bring the 30-year mortgage rates down to around 6%,” Yun says. “The usual spread between the 10-year Treasury yield and the 30-year mortgage rate is between 150 to 200 basis points, rather than the current spread of 300 basis points.”

First-time buyer challenges

First-time buyers looking to purchase a typical home during the third quarter of 2022 continued to feel the impact of housing’s growing unaffordability. For a typical starter home valued at $338,700 with a 10% down payment loan, the monthly mortgage payment rose to $1,808 – nearly identical to the previous quarter ($1,807) but an increase of almost $600 (49%), from one year ago ($1,210).

First-time buyers typically spent 37.8% of their family income on mortgage payments, up from 36.8% in the previous quarter. A mortgage is considered unaffordable if the monthly payment (principal and interest) amounts to more than 25% of the family’s income.

A family needed a qualifying income of at least $100,000 to afford a 10% down payment mortgage in 59 markets, up from 53 in the prior quarter. Yet, a family needed a qualifying income of less than $50,000 to afford a home in 17 markets, down from 23 in the previous quarter.

For those looking for the good news about today’s real estate market. A bit of a deep dive, about 60 minutes worth but excellently delivered. Three main facts tell us it’s not all doom and gloom. Combine them with the time of year and the general fear that has most buyers/sellers on the sidelines, spells opportunity. (40:00). We can help should you decide to take advantage of today’s market.

Historical trends, what happens after quantitative tightening (12:00)

Demographics, there’s a lot of millennials (24:50)

Inventory levels, yes they are still historically low (22:00)

Access this weekly report for real-time data on residential market activity across the Bright MLS footprint. October 17, 2022 Lisa Sturtevant, PhD

Here are the highlights for the week ending October 16, 2022:

Inventory continues to increase throughout the Bright footprint. The average number of active listings during the week ending October 16 was up 17.5% compared to the same week a year ago. Active listings edged up 0.9% compared to last week, which is the second weekly increase in a row. Despite these increases, overall supply across the region remains very low.

Market activity is still below 2019 levels as buyers and sellers continue to remain on the sidelines. On the buyer side, both closed sales and new purchase contracts were down significantly compared to last year at this time and were even lower than before the pandemic. Closed sales this week were about 14% lower than the same week during 2019, while the number of new purchase contracts tracked 22% lower than during the same week in 2019.

There was a slight uptick in both new purchase activity and new listings compared to a week ago. Typically, both the number of new purchase contracts and new listings decline during the second week of October. This year, however, there were slight increases, with new purchase contracts 2.1% higher than a week ago and new listings up 3.0% week-to-week. These weekly increases could indicate some buyers and sellers are starting to act in anticipation of higher mortgage rates later this fall.

Homes are still selling relatively quickly. The median days on market was 15 during the week ending October 16, which is up four days compared to last year and is one day longer than a week ago. The median days on market is still much lower than 2019, when homes typically took 25 days to sell.

Interest rates for the average 30-yr, fixed-rate mortgage according to Freddie Mac’s PMMS hit:

4% in March 😟 5% in April 😰 6% in early-September 😨 7% (well, almost) in late-September 😱

The slowdown continues, but we have yet to see the impact of the most recent (massive) jump in mortgage rates on homebuyer demand.

August existing home sales dropped for the 7th straight month. Price growth decelerated further to “just” 8% YoY. [Source: Realtor.com]

Meanwhile, pending sales for August dropped 2% MoM and 24% YoY. The NAR now forecasts existing home sales to fall 15% YoY in 2022, with new home sales down 21% YoY. [Source: NAR]

Case-Shiller Index

Home price growth slowed to 15.8% YoY in July, from 18.1% YoY in June. That may not seem like much, but it’s the biggest 1-month drop in the index’s history.

Case-Shiller is the gold standard for home price appreciation because it tracks the sales prices of very similar homes across 20 big cities. It’s an ‘apples to apples’ comparison. But that accuracy comes at a cost…the data is 2 months old by the time we get it.

Mortgage Market

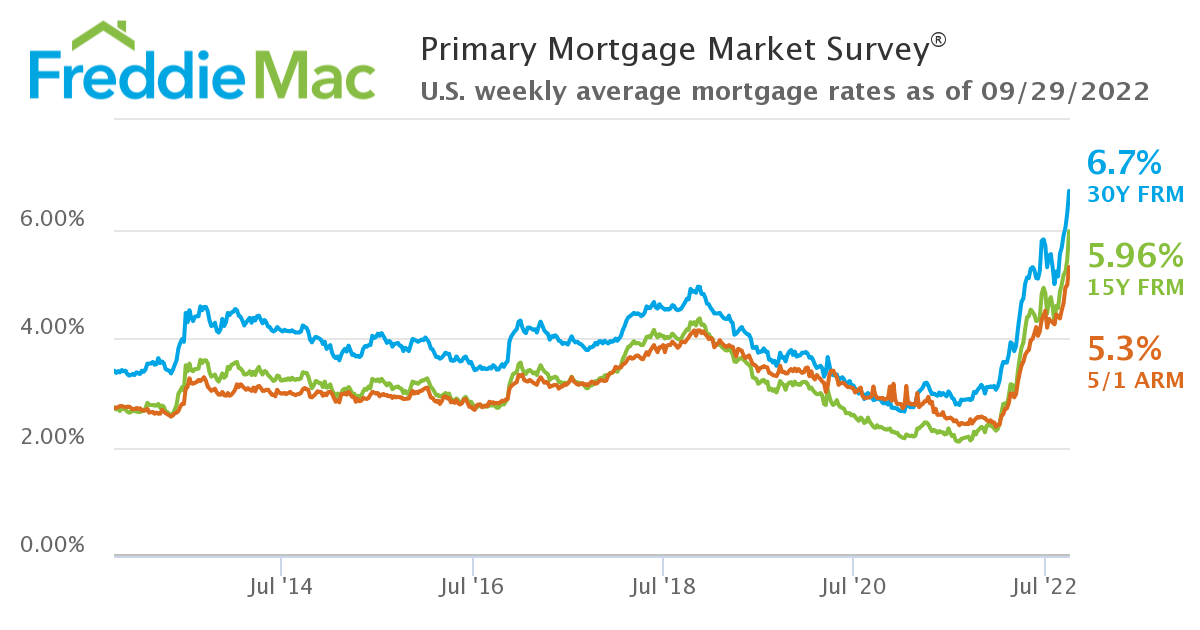

An extremely volatile week for the bond market (after the Fed raised rates 75bps) saw 30-year, fixed-rate mortgages briefly exceed 7% [with no points], before dropping back to around 6.75%. [Source: Mortgage News Daily]

Freddie Mac’s closely watched PMMS survey saw the interest rate on the average 30-year, fixed-rate mortgage climb to 6.7%. Keep in mind that this figure includes an average 0.9 points purchased. Without those points, the rate would have been at/ahead of 7%.

Still a Seller’s Market

Demand is falling and inventory has risen, but in most markets, well-priced homes are still selling very, very quickly.

In fact, the average Days on Market for sold properties has only edged up from 14 (in June & July) to 16 in August. In 2011 that figure was 96! Looked at another way, 81% of homes sold in August had been on the market less than a month.

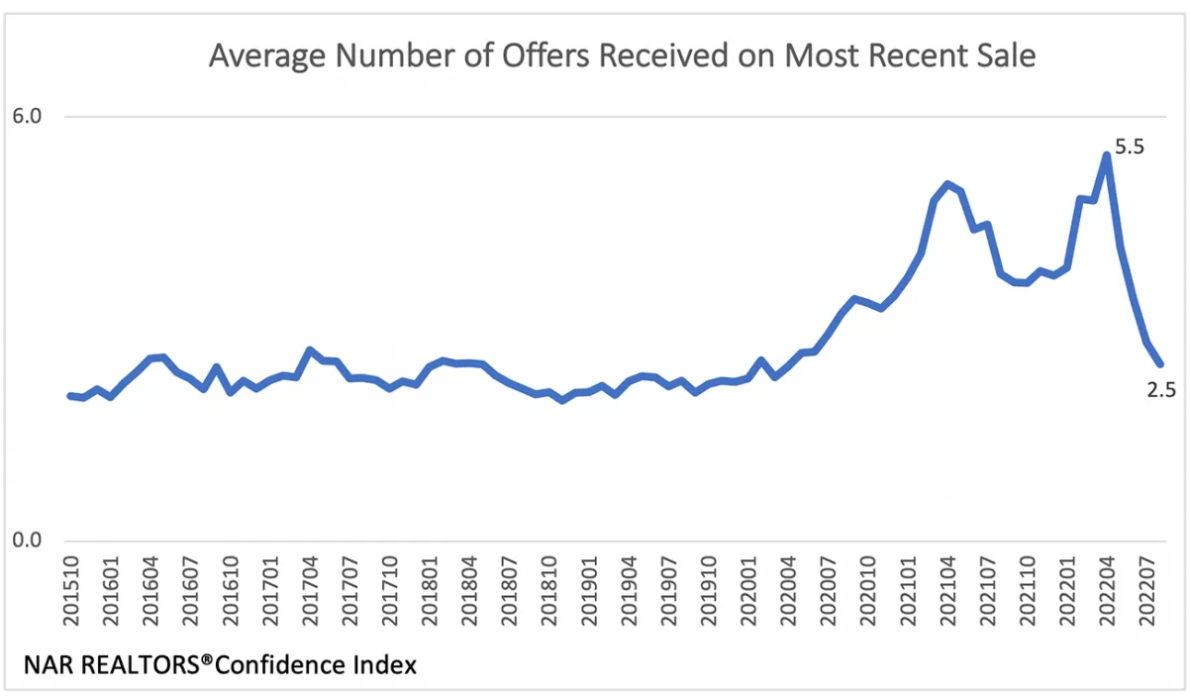

That said, the average number of offers received for each property sold has plunged from a frenzied 5.5 in April 2022 to 2.5 in August. That’s actually getting pretty close to “normal” pre-pandemic levels of competition.

National Housing Stats

They Said It

“Success demands singleness of purpose. You need to be doing fewer things for more effect instead of doing more things with side effects. It is those who concentrate on one thing at a time who advance in this world.” — Gary Keller, The One Thing

“Our house is clean enough to be healthy and dirty enough to be happy” — Robyn Griggs Lawrence

Inspiration

The average duration of homeownership in the US is around 12 years. So if someone in your sphere of influence (SOI) bought a home in the last few years, there’s no reason to actively stay in touch with them, right? Wrong. Take the inverse of 12 (that’s 1/12) and you get 8.3%.

This means that, mathematically, 8% of your SOI is going to move in the next year…for reasons that you (and often they) couldn’t have predicted. Hockey legend Wayne Gretzky said “you miss 100% of the shots you don’t take.” In real estate, you probably lose 80–90% of the past clients that you don’t stay in contact with.

Weekly Housing Market Update – 9/16/22 – Chief NAR Economists, Danielle Hale, not only forecasted the rate hike she also highlights her thoughts around 2:35 of the video regarding home sellers and home buyer.

If you’re following along with the news today, you’ve likely heard about rising inflation. You’re also likely feeling the impact in your day-to-day life as prices go up for gas, groceries, and more. These rising consumer costs can put a pinch on your wallet and make you re-evaluate any big purchases you have planned to ensure they’re still worthwhile.

If you’ve been thinking about purchasing a home this year, you’re probably wondering if you should continue down that path or if it makes more sense to wait. While the answer depends on your situation, here’s how homeownership can help you combat the rising costs that come with inflation.

Homeownership Offers Stability and Security

Investopediaexplains that during a period of high inflation, prices rise across the board. That’s true for things like food, entertainment, and other goods and services, even housing. Both rental prices and home prices are on the rise. So, as a buyer, how can you protect yourself from increasing costs? The answer lies in homeownership.

Buying a home allows you to stabilize what’s typically your biggest monthly expense: your housing cost. If you get a fixed-rate mortgage on your home, you lock in your monthly payment for the duration of your loan, often 15 to 30 years. James Royal, Senior Wealth Management Reporter at Bankrate, says:

“A fixed-rate mortgage allows you to maintain the biggest portion of housing expenses at the same payment. Sure, property taxes will rise and other expenses may creep up, but your monthly housing payment remains the same.”

So even if other prices rise, your housing payment will be a reliable amount that can help keep your budget in check. If you rent, you don’t have that same benefit, and you won’t be protected from rising housing costs.

Use Home Price Appreciation to Your Benefit

While it’s true rising mortgage rates and home prices mean buying a house today costs more than it did a year ago, you still have an opportunity to set yourself up for a long-term win. Buying now lets you lock in at today’s rates and prices before both climb higher.

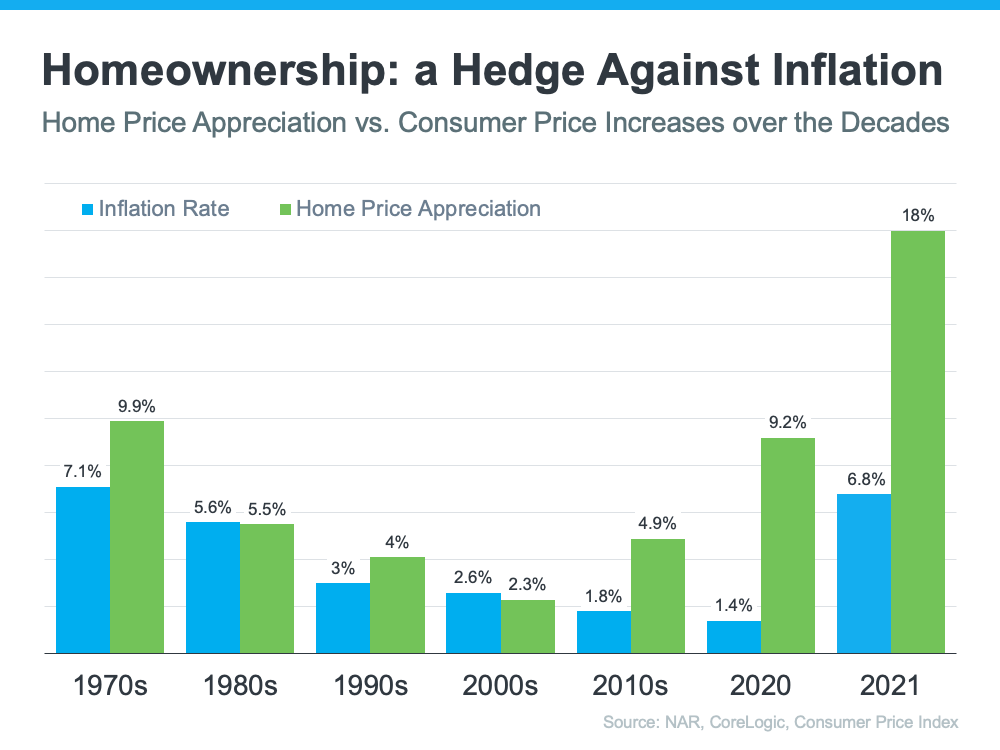

In inflationary times, it’s especially important to invest your money in an asset that traditionally holds or grows in value. The graph below shows how home price appreciation outperformed inflation in most decades going all the way back to the seventies – making homeownership a historically strong hedge against inflation (see graph below):

So, what does that mean for you? Today, experts say home prices will only go up from here thanks to the ongoing imbalance in supply and demand. Once you buy a house, any home price appreciation that does occur will be good for your equity and your net worth. And since homes are typically assets that grow in value (even in inflationary times), you have peace of mind that history shows your investment is a strong one.

Bottom Line

If you’re ready to buy a home, it may make sense to move forward with your plans despite rising inflation. If you want expert advice on your specific situation and how to time your purchase, let’s connect.

Federal Reserve Chair Jerome Powell testifies about monetary policy and the state of the economy before the House Financial Services Committee on Wednesday. Powell reiterated the Fed is gearing up to raise interest rates this month.

Federal Reserve Chair Jerome Powell said on Wednesday the central bank is on track to start raising interest rates this month — likely by a quarter percentage point — in an effort to combat inflation, which is the highest it’s been in nearly 40 years.

But the Fed will proceed with caution, Powell told the House Financial Services Committee, as Russia’s invasion of Ukraine adds more uncertainty to the economic outlook.

“The economics of these events are highly uncertain,” Powell said. “So far, we’ve seen energy prices move up further and those increases will move through the economy and push up headline inflation, and also they’re going to weigh on spending.”

The average price of gasoline in the U.S. approached $3.66 per gallon on Wednesday. Rising energy prices have been a significant driver of annual inflation, which hit 7.5% in January – the highest level since 1982.

Powell says it’s too soon to tell on Ukraine

Powell said it’s too soon to know how large or long-lasting price increases tied to events in Ukraine will be, so he and his colleagues on the central bank’s rate-setting committee are prepared to be flexible.

“We’re never on auto-pilot,” Powell said. “Those of us on the committee have an expectation that inflation will peak and begin to come down this year. And to the extent that inflation comes in higher or is more persistently high than that, then we would be prepared move more aggressively.”

Forecasters expect the Fed to impose additional interest rate hikes later this year in an effort to cool red-hot consumer demand, which has outstripped supply and driven prices sharply higher.

The profit on a typical home sale last year was just over $94,000, an increase of 45% from the profit in 2020 and 71% from pre-pandemic profits.

About 42% of homeowners were considered equity-rich at the end of last year

The amount of tappable equity (equity above the 20% usually required by lenders to back a mortgage) grew by $2.6 trillion last year to a record total of $9.9 trillion.

The stunning jump in home values over the course of the Covid-19 pandemic has given U.S. homeowners record amounts of housing wealth. What they choose to do with it could have impacts on the broader economy.

Annual home price gains averaged 15% in 2021, up from 6% in 2020, according to CoreLogic. Strong pandemic-driven demand, record low supply and record low mortgage rates conspired to create those hefty gains. Bidding wars are now the norm, and desperate buyers are competing with investors who want to cash in on the hot market. The upward trend is continuing, despite winter being historically the slowest season for housing.

“While we expect this year’s buyers will eventually see some relief from the 2021 frenzy, home shoppers continue to face challenging conditions in the early days of 2022,” said Danielle Hale, chief economist for Realtor.com. “In fact, last week’s home price and time on market trends suggest competition intensified.”

A year before his death, he launched the Poor People’s Campaign to fight job and housing inequality, among other issues. Historians say the Poor People’s Campaign and the Chicago Open Housing Movement laid the groundwork for the 1968 Fair Housing Act

Trikosko, Marion S.,/Library of CongressBY MARIAN MCPHERSONJanuary 15, 2018

This post was last updated Jan. 14, 2022. – Inman News

Although Martin Luther King, Jr. is most remembered for his struggle to secure voting rights and stop segregation, the civil rights icon’s dream of racial equity reached far beyond integrated public life — it also included economic security and housing rights for the millions of minority and low-income Americans who’d been relegated to their cities’ under-resourced neighborhoods and housing projects.

King began planting the seeds of what would become the Poor People’s Campaign in Chicago, where thousands of Black Chicagoans struggled with job and housing insecurity — something they’d hoped they escaped during the Great Migration, the term used to describe a decades-long exodus from the fields of the South to the factories of the North.

Although some Black people found great success in Chicago, Detroit, New York City and other similar places, many more found the only thing that changed in their life was their address.

“We are here today because we are tired,” Dr. King said, according to a transcript of a speech he made at Chicago’s Soldier Field. “We are tired of paying more for less. We are tired of living in rat-infested slums … We are tired of having to pay a median rent of $97 a month in Lawndale for four rooms while whites living in South Deering pay $73 a month for five rooms.”

“Now is the time to make real the promises of democracy,” he added. “Now is the time to open the doors of opportunity to all of God’s children.”

According to articles by HuffPost and NPR, Dr. King spent much of 1966 in Chicago, even moving his family to an apartment on the city’s predominately Black west side. There, King and Southern Christian Leadership Conference (SCLC) launched the Chicago Open Housing Movement, whose goals included the rehab of public housing, increasing the supply of affordable housing, pushing for diversity and integration in businesses and unions, a $2 minimum wage and the abolition of wage garnishment.

Over the course of the year, King and SCLC activists held citywide rallies, planned demonstrations in front of real estate brokerages and marched into Chicago’s all-white neighborhoods, which were met with violent reactions from the city’s white residents. “Well, this is a terrible thing,” King said in a soundbite acquired by NPR. “I’ve been in many demonstrations all across the South, but I can say that I have never seen, even in Mississippi and Alabama, mobs as hostile and as hate-filled as I’m seeing in Chicago.”

Eager to quell the violence, Chicago’s mayor, Richard J. Daley, agreed to meet with King and other activists in August 1966 to work out an agreement, which included building future public housing with “limited height requirements,” and requiring the Mortgage Bankers Association to make mortgages available regardless of race.

King hailed the agreement ‘‘the most significant program ever conceived to make open housing a reality,’’ but tempered his assessment by recognizing it as only “the first step in a 1,000-mile journey.’’

The next year, King went back to the South and began planning the Poor People’s Campaign, which was built from his experiences in Chicago the year before. He and the SCLC began creating a blueprint for economic and housing equity that addressed the systems and policies that kept minority and low-income communities behind the eight ball.

“This is a highly significant event,” King told the SCLC in November 1967, according to an archive at Stanford’s King Institute. “[This] the beginning of a new co-operation, understanding, and a determination by poor people of all colors and backgrounds to assert and win their right to a decent life and respect for their culture and dignity.”

He garnered support from civil rights leaders in American Indian, Puerto Rican, Mexican American, and poor white communities and began planning another March on Washington to demand jobs, unemployment insurance, a fair minimum wage, and education for adults and children. “It’s as pure as a man needing an income to support his family,” King said.

King was assassinated before he could finish planning the demonstration; however, other SCLC leaders and his wife, Coretta Scott King, banned together and finished planning the march, which took place on Mothers’ Day 1968. After the initial demonstration, protestors pitched tents on the Mall in Washington and lobbied for fair employment and housing policies until their park permit expired a month later.

Even though the campaign was largely unsuccessful in making widespread change — they did secure free food surplus distribution to 200 counties — historians say the Poor People’s Campaign and the Chicago Open Housing Movement laid the groundwork for the 1968 Fair Housing Act, which ensures that all Americans have access to equal housing opportunities and outlaws discrimination based on an individual’s race, color, religion, sex, national origin, disability or familial status.

“And we have to continue in the legacy of MLK and the civil rights movement and the legacy of abolition movements of before,” said Paige May, a Chicago resident who spoke to NPR after an event to celebrate MLK.

“We have a lot of work to do, but it’s also — it feels like a day that’s celebratory in a lot of ways, right? But in the sphere of struggle and resistance.”